Collectibles: A Remarkably Durable Asset Class

Collectibles: A Remarkably Durable Asset Class

A deep dive on the infrastructure, formats, and markets shaping the future of collectibles

May 2026

Collectibles, as an asset class, are unkillable. The industry has survived the Great Depression, two World Wars, the dot-com crash, the GFC, COVID, and the current macro cycle, and has come out larger every single time. The category has compounded for almost a century in spite of itself, with no standardized infrastructure, no centralized price discovery, and no real financial plumbing. What’s happening now is that all three are finally being built at once.

At Will Ventures, we’ve been spending the last few months going deep on the market.

We think collectibles are in the middle of a big transition. The same kind of transition that turned other products like fine art and wine into legitimate financialized markets in earlier generations.

We have 3 beliefs that we’ll discuss in this piece:

- The trading card playbook is a template, not the destination. The next decade of category-defining companies in collectibles will be built in watches, memorabilia, toys, and a handful of others. Most capital is still chasing cards.

- Digital repacks are one of the most important commercial innovations in the category in 30 years and also very exposed to regulatory disruption. There is significant downside risk, but this model can be applied to other industries.

- The trust layer (grading, authentication, vaulting, and lending) will produce huge outcomes in other categories.

Part 1: The Maturity Curve

Every asset class went through some version of the same transition. We think this is the most useful framing for where collectibles are now.

Take art. For most of the 20th century, fine art was bought by people who liked art, displayed by people who could afford to display it, and traded through dealers who knew everyone. There was no public price for a piece, no way to borrow against one, no index. Then in the 1970s and 1980s, Sotheby’s and Christie’s published auction results consistently enough that comps became visible. Specialist art lenders emerged. Independent appraisers got professionalized. Insurance products got standardized. By the 2000s, fine art had become a real asset class that institutional investors could allocate to and family offices could lend against.

Wine went through the same transition between 1980 and 2010, with the rise of en primeur futures, Liv-ex as a centralized exchange, Robert Parker scoring as a near-universal grading scale, and bonded warehousing as standardized custody.

We see a similar pattern across these assets. A category becomes a real asset class when four pieces of infrastructure exist at once: standardized authentication, reliable price discovery, custody and provenance, and financing and instruments. When all four exist, the category gets repriced upward, often dramatically, because it can absorb a much wider pool of capital. Buyers no longer need to be domain experts. Lenders no longer need to underwrite each transaction from scratch. Institutional allocators can finally buy in.

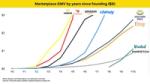

Trading cards are roughly seven years into this transition. PSA’s grading scale is universally accepted. CardLadder and Market Movers provide real-time comps. Vaulting and digital repacks have built a custody layer. Alt and others have built the financing layer. Cards are the first collectible category where all four pieces exist simultaneously, and you can see the result in monthly trading volume, which is roughly 50x what it was in 2018.

Every other major collectibles category is missing at least two of the four pieces. Watches have decent custody and a real marketplace, but no standardized grading scale and limited lending. Game-worn memorabilia is missing all four. Toys have demand and content but no grading premium and no real secondary market for graded inventory. Handbags have credible authentication but no grading, no vaulting, and no lending at scale. Wine is the most mature outside of cards, with all four pieces present but most still operating at meaningful friction.

The companies that win the next decade in collectibles will be the ones building the missing infrastructure for categories that aren’t cards.

Part 2: The market today and key stakeholders

The global collectibles market is massive and sits somewhere between $320 billion and $600 billion (the global video game market is ~$300B), depending on who’s measuring and what they’re including. The wide range itself tells you something about the lack of structure across the industry.

The TCG market (Pokémon, Magic: The Gathering) was roughly $7.5 billion in 2025. Sports cards add another $13 to $15 billion on top of that. Combined, the trading card market is $20B+ and growing at a healthy clip.

Beyond cards, toy collectibles, blind boxes, designer figures, and the whole Labubu / Pop Mart phenomenon, are growing at nearly 11% annually, driven heavily by Asia-Pacific and the “kidult” demographic that now accounts for over a third of the toy market.

The collectibles ecosystem is convoluted and full of different stakeholders. Let’s take a look at the different players in the sports and trading card market for example.

IP Holders sit at the top. Leagues, entertainment franchises, and player associations license their IP and collect royalties on every card and sticker produced. That’s somewhere between $500 million and $1 billion a year across sports, entertainment, and TCG. For decades, IP holders were perfectly happy cashing royalty checks while the rest of the chain captured the real upside, but that dynamic is changing.

Manufacturers make the product. Topps (now Fanatics), Panini, and Upper Deck are the biggest names there. The total manufacturing layer is $4 to $5 billion globally. Manufacturers are now trying to vertically integrate and build a full stack: pack rips, marketplace, portfolio management, etc. all under one roof.

Grading and Authentication is quietly one of the best businesses in the ecosystem. PSA, Beckett, CGC, and SGC assign condition grades on a standardized scale. Graders are an extremely important part of the value chain - a PSA 10 Pokémon card can fetch 5 to 10x what a PSA 9 of the exact same card sells for. In 2025, 26.8 million cards were graded across major companies, up 32% year over year. PSA accounted for 19 million+ of those, grading more than 90,000 cards daily. Collectors, PSA’s parent company, raised at a $4.3 billion valuation in 2022 and has since rolled up SGC and Beckett, consolidating roughly 80% of the card grading market under one roof.

Marketplaces are where most collectors are getting their collectibles. eBay did over $10 billion in collectibles GMV in 2025, with trading cards as the single biggest driver of GMV growth for nine straight quarters. Add Goldin, Fanatics Collect, Alt, Whatnot, and the long tail, and secondary marketplace volume probably exceeds $15 billion a year. Live commerce has been a big innovation in the last 10 years, with breakers on Whatnot and Fanatics Live blending shopping with entertainment in a way that looks more like Twitch than eBay.

Financial Instruments and Repacks are the newest part of the stack. We’ll cover this in more detail later. Fractional ownership, lending (Alt Advance lets you borrow against vaulted cards at 9 to 10% APR), and digital repacks (Triumph, Courtyard, Arena Club, etc.) are all building new on-ramps into collectibles. This layer is probably $1 billion today and growing fast. The idea around lending is simple: if you can borrow against other assets, you should be able to borrow against your card collection. Digital repacks have done a great job taking less desirable inventory and generating liquidity for them.

This stack exists in other categories beyond cards as well, though the depth of the value chain is more limited in other areas.

Okay, now that we understand the major parts of the ecosystem, let’s talk about what’s driven the growth that has pushed collectibles from a niche hobby to a legitimate asset class.

A standard explanation for the current boom goes something like: COVID, stimulus checks, nostalgia, low rates. That’s part of the story but it’s incomplete. Four structural shifts have compounded over the last decade.

Liquidity and transparency: CardLadder and similar companies give collectors real-time comps on almost any card. Online marketplaces eliminated geographic friction in what used to be a deeply local hobby. Grading capacity has roughly 5x’d. The asset class has moved from “I think this is worth something” to “I know exactly what this is worth right now.”

Demographics and wealth transfer: The kids who collected Pokémon and ripped basketball packs in the late ‘90s and early 2000s now have real disposable income and a deep emotional connection to the IP. Roughly 60% of US collectors are now between 25 and 45. High-net-worth collectors allocate around 20% of their wealth to collections and the growth will continue to compound.

Content as a flywheel: Whatnot did roughly $6 billion in GMV in 2025, doubling year over year. DeepPocketMonster has 4 million followers across platforms ripping packs on stream. Card opening went from a solitary basement activity to one of the most engaged-with content categories on the internet. Content turns collectibles into a recurring, social, top-of-funnel acquisition channel rather than a niche hobby that requires hand-to-hand evangelism.

Format innovation: Digital repacks, live breaks, blind boxes, fractional ownership, and instant-liquidity vaults have all been invented or scaled in the last five years. Each format independently increases the velocity of capital and stacked on top of each other, have rewritten unit economics of the entire industry.

What’s interesting is that we think many of these shifts have significant runway left. Demographics, wealth transfer, and format innovation will only continue and we think we’re still in the early innings of this industry.

Part 3: Cards as proof of concept

By now, many of you may be familiar with the story of trading cards and sports cards and their recent growth. The point of this section is to discuss what’s driven the growth and how we think the success of cards can translate to other collectibles categories.

Grading is an unsung need and profit pool

As mentioned above, one company, Collectors Holdings now controls roughly 80% of the card grading market. The margins are extraordinary and capacity is the real constraint. PSA, the largest brand under Collectors, has built a brand that has a tremendous moat.

Collectors CEO Nat Turner has re-vitalized the PSA business. The business already had significant momentum, mostly driven by the fact that a PSA 10 card can fetch 5 to 10 times what a PSA 9 of the same card sells for. But, PSA has quietly evolved from a simple grading company into the trust, data, and infrastructure layer that underpins the financialization of cards.

Effectively, the grading scale is what makes the asset class function. Without it, you have no comps, no lending, no digital repacks, no derivatives. With it, you have all four. Whoever builds the equivalent in another category captures the same kind of structural margin and the same kind of moat. We’ll come back to this in Part 4.

Breaking is now a media business, and the media business is the interesting part

A “break” is a group purchase of a sealed product. A breaker buys a $500 hobby box, sells 30 spots at $20 each, opens the packs live, and whoever’s spot has the big hit walks away with the card. It feels part like a lottery, part like QVC, and part like Twitch.

The economics are good. Whatnot takes about 10–11% of GMV including payments. Breakers buy at wholesale, sell spots at 15 to 40% above MSRP, and clear 15 to 25% net margins on the spread. Top full-time breakers can clear $500,000 a year and breaker networks like WeTheHobby, which started as a one-person operation in 2021 and now has 160-plus employees, are doing $15m+ in annual revenue at 20% margin.

WeTheHobby has effectively become a vertically programmed media company that happens to monetize through cards, with dedicated channels by sport, on-air talent, podcast operations, original IP, and the leverage to negotiate exclusive allocations from manufacturers. The most successful card retailers in the country, like Layton’s, reportedly do up to 90% of their revenue through breaks.

The question we keep coming back to: do platforms tolerate aggregators long-term, or prefer to own talent relationships directly? Twitch and YouTube spent the last decade neutering MCNs once creators figured out they didn’t need them. We think the same fate awaits most generic breaker networks. The ones that survive will look like sports media companies with proprietary IP, exclusive allocations, and direct relationships with manufacturers and IP holders.

The format is also migrating into adjacent categories. We’ve seen breaks for Pop Mart cases, sealed Funko, Magic boxes, watches, sneakers, and luxury goods. The constraint is that breaking only works when the underlying product has high variance, transparent comps, and meaningful chase items. Cards check all three. Toys and blind boxes check most of them. Watches and high-end sneakers check fewer. Our prediction: breaking goes deep into toys and TCG-adjacent categories and stays niche in watches and luxury.

Digital repacks: An entirely new format that has re-written unit economics

Digital repacks are one of the most important commercial innovations in the collectibles industry in 30 years. They didn’t exist three years ago and are now arguably the highest-velocity business model in the entire space.

The mechanic is straightforward. A platform vaults a pool of pre-graded cards, publishes the odds and checklist, and sells digital “packs” online ranging from $10 to $10,000 plus. You buy a pack, see your card revealed instantly, and decide whether to ship, vault, or sell it back to the platform at roughly 90% of fair market value. Most users sell back instantly. Cards transact 8 to 10 times before any single one is redeemed. The platform takes about 10% of GMV every time.

The most useful number we’ve heard in the category: roughly $1 of platform inventory generates around $10-20 of GMV per month. That is a unique e-commerce ratio. eBay does roughly $0.10 of GMV per dollar of inventory across its marketplaces. Amazon’s third-party marketplace does maybe $0.40. Digital repacks, at $10-20, are operating in a different economic universe.

Two strategic camps have emerged.

The collector camp (Courtyard, Arena Club, Trove): premium positioning, athlete and team partnerships, collector tools, vaulting, and category expansion. Courtyard launching watches is the early read on whether the format works outside of cards.

The engagement camp (Triumph, Packz, Catchback Cards): aesthetic and pacing closer to mobile gaming and DFS than collecting. Faster reveals, smaller tickets, gamified mechanics. The user base overlaps heavily with sports betting and social casinos.

Three things flow downstream. First, repacks pull demand forward for grading. Every card has to be slabbed first, which is part of why PSA processed 19 million submissions last year. Second, they make vaulting table stakes, not optional. The vault is the wedge, the same way custodial infrastructure was the wedge in crypto. Some companies are doing this directly and others are doing it through 3rd parties. Third, repacks create a new liquidity layer for previously illiquid mid-value cards, which had been too cheap to auction and too good for raw eBay listings.

Now here is where we have some concerns.

Mechanically, a buy-and-sell-back digital pack is hard to distinguish from a chance-based wager with a fixed house edge. That mechanic is well-known to gaming regulators and the dollar volumes are now getting too large for state attorneys general and gaming commissions to ignore. The participants also skew young and the skill-versus-chance line is fuzzy for buy-back mystery boxes.

We think operators that publish full odds, gate underage participation, set per-user spend limits, and lean into responsible-spending features will be in much better shape when scrutiny arrives. Operators leaning into casino-style retention loops, hidden odds, or DFS-style aesthetics are going to be the test cases. Our best prediction is that regulators will increasingly scrutinize digital repacks in the coming few years, especially if the underlying card market softens. At that point, the companies that will face more scrutiny will be the ones that cannot credibly distinguish their product from a lottery, platforms without transparent odds disclosure, age verification, deposit limits, or a clear collectibles-first (rather than wager-first) value proposition.

To be clear, we are still long this format.

The fact that consumers are guaranteed to get a physical asset at a floor price and that this dynamic is similar to the physical experience a card collector has at a show, gives us confidence this model can exist without regulatory scrutiny. Furthermore, the unit economics are too compelling for it to disappear, and the format is too useful to the rest of the value chain to be banned outright. But the operators that come out the other side will grow very responsibly and make product decisions that are good for the user and the industry at large.

Part 4: Where the next category-defining companies will actually be built

We think the next decade of category-defining companies in collectibles will be built in the categories sitting one or two steps behind cards on the maturity curve.

For each category below, the operative question is the same: which of the four maturity-curve pieces (grading, price discovery, custody, financing) are missing, who has the right to build them, and what do the resulting businesses look like at scale.

Game-worn memorabilia

The emotional resonance of game-worn memorabilia is arguably the highest in the entire collectibles stack. However, the infrastructure to support it is perhaps the lowest. There are 3 core problems.

Supply is opaque and relationship-driven: Topps prints millions of cards a year. An athlete wears one jersey per game. Across the major US leagues, you’re looking at a few hundred thousand game-worn items a year, and most never reach the open market. They stay with the athlete, route through equipment managers with private networks, go to charity auctions, or get gifted. Sourcing is hand-to-hand combat that takes years.

Authentication is technologically primitive: Fanatics Authentic, Beckett, Meigray, and MatchWornShirts are names that are deep in the space. The actual workflow at most of these companies however still requires significant human intervention. Computer vision authentication, which can match a jersey to a specific game from broadcast footage in seconds based on stitching patterns, sweat and dirt placement, fabric wear, etc., doesn’t exist at scale yet. We think someone will build that technology soon.

There is no grading scale: “Excellent condition” is a narrative. Cards have a 1-to-10 scale that the entire market trusts; that scale is what enables price discovery, lending, and digital repacks. Memorabilia has nothing like it. A photo-matched jersey worth $500,000 and a non-photo-matched jersey of the same player from the same season worth $50,000 will be described in the same auction catalog using effectively identical adjectives.

The bull case is interesting. Unit values are higher than cards and supply is structurally scarce in a way cards never will be. Buyers are wealthier and emotional resonance is highest. The bear case is that all four maturity-curve pieces have to be built more or less from scratch, and the people who can build them need a combination of skills (deep league relationships, authentication expertise, and auction operations) that almost nobody has.

Watches

Watches are an interesting category. The luxury watch market is $33 billion for primary and roughly $22 billion for pre-owned. Chrono24, Bezel, and others have built credible online marketplaces. Furthermore, brand-run certified pre-owned programs from Rolex, AP, Patek, and others have given collectors more confidence on the highest-end inventory. Liquidity is decent at the top of the market but gets thin fast as you move down.

What’s missing is the same thing that was missing in cards 10 years ago: a universally accepted, standardized grading scale. Watch authentication today is a mix of brand certifications, individual experts, and platform-specific authentication layers. None of it converts cleanly into a number the market can underwrite.

This matters because the absence of grading is the actual constraint on the watch market becoming an asset class. Buyers need expertise and lenders need to underwrite each transaction from scratch.

We think a PSA-equivalent for watches is an obvious company that doesn’t yet exist. Whoever builds a credible 1-to-10 scale, with the brand equity and process discipline to make a “Grade 9 Patek” mean the same thing to every dealer, lender, and collector globally, becomes a critical piece of the value chain.

There are some challenges: watches have moving parts, the market is more mature than cards were in the early 2010s, and brand certification programs exist. But remember, TCG manufacturers also saw PSA as a competitor before realizing their value. We think the same pattern will play out in watches, and the window to build this is now.

Toys and blind boxes

Pop Mart is one of the more impressive consumer companies built in the last decade. The brand grew 3x year over year to $5B+ in revenue last year. Labubu has crossed over from Asia-Pacific into the US, EU, and LATAM. The unboxing-on-social loop is the same behavioral mechanic that drives breaking on Whatnot, and it is producing the same kind of viral demand.

While demand has been solved, there is still ample opportunity on supply, secondary markets, authentication, and price discovery.

Grading: CGA grades action figures and Funko Pops. The problem is that, unlike cards, a graded toy does not consistently command a meaningful premium over an ungraded one. Until that changes, throughput will likely stay capped. Whoever builds a grading scale that the market actually pays a premium for unlocks the entire downstream stack (lending, repacks, indices) for toys.

Cross-border secondary markets: Most interesting toy supply originates in Asia, and most new demand is in the US and EU. The cross-border arbitrage is real and currently captured by a fragmented set of resellers, eBay sellers, and Discord-organized group buys. Someone is going to consolidate this with proper authentication, customs handling, and unified pricing. The resulting business may end up looking a lot like StockX for toys.

Pricing data: There is no CardLadder for toys. One interesting case is ghostwrite, the collectible toy business that partners with leading IP and does a combination of limited drops and blind boxes. They have built their business on blind dutch auction pricing - this mechanism has created transparency for both primary participants and future secondary buyers. We think someone will build a data asset that allows comparisons across products and standardizes price discovery.

We are bullish on toys as a venture-investable category; we think the right toy-specific platform with a credible authentication and pricing layer can become a massive outcome.

Part 5: The Financial layer is a big, underbuilt opportunity

If we had to point at one structural shift that would do the most to financialize collectibles over the next decade, it would be the maturation of the lending and capital layer.

Cards are increasingly treated like a real asset class because the financial plumbing has caught up. Alt offers loans up to 40% of total card portfolio value. PWCC has a $175 million credit facility with WhiteHawk. Collateral Finance Corporation lends against vintage cards alongside precious metals. The category now has fixed and variable rate options, instant cash advances against vaulted inventory, and a real secondary market for the underlying loans.

There is essentially nothing of comparable scale in watches, memorabilia, toys, handbags, wine, sneakers, or comics. Every one of these is a billion-dollar-plus market with assets that hold value, can be vaulted, and can be authenticated, and yet there is no real lending product against any of them.

Across many of these categories, unit values are higher than cards. Assets are just as durable. And the buyer base is wealthy so default rates are likely to be very low.

The right way to build is category by category, partnered with the dominant authentication and vaulting player in each vertical. Horizontal lending platforms across all collectibles will lose to vertical specialists who own the trust layer in a single category first. Underwriting expertise scales by category, not horizontally. The winning model is to build the dominant lending product in one category, integrate tightly with the grading and vaulting infrastructure, and only later expand sideways.

We expect to see two or three category-specific lending platforms reach significant scale in the next five years. We think the first will probably be in watches and the second will probably be in memorabilia, contingent on someone solving the grading problem.

Part 6: International is another massive expansion opportunity

The US is roughly 55% of global trading card value. Europe is 25%. Asia-Pacific is 20–25%. LATAM and MENA are the rest. Most category-defining collectibles platforms we’ve discussed so far are US-first. We think that will change. Let’s look at a few of these geographies.

Asia-Pacific: Japan is already a $2 billion-plus market, the largest outside of the US, with deep TCG roots and a mature collector base. Local auction houses, marketplaces, and grading services already exist. In China, the collectible behavior is built around new IP (Pop Mart, Kayou) rather than legacy IP, and the platforms that win there will look very different from PSA or Whatnot. Counterfeiting is a structural problem that creates a durable opportunity for a trusted authentication brand. South Korea is also emerging fast, with a young, mobile-first collector base.

Each market has its own payment rails, dominant social platforms, counterfeiting risks, IP landscape, and buyer demographics. The winners are likely to start as regionally native companies with proprietary IP and authentication relationships. We also don’t think the infrastructure stack in Asia will be rebuilt the same way it was in the US. Payments, social distribution, and commerce are already well integrated, which compresses the time it takes for a category to financialize.

Latin America: Anecdotally one of the fastest-growing collector communities in the world, especially Mexico, Brazil, and increasingly Argentina and Colombia. Today the activity sits in Discord, WhatsApp, Mercado Libre, and a small handful of regional Instagram-driven platforms. This fragmentation we think will change. We expect one platform to consolidate most of the activity, with payments, centralized inventory and pricing, and build native social and community features. We think there’s a real chance the LATAM winner becomes a multi-billion dollar company without ever entering the US market.

India: The collector base today is materially smaller than in other markets despite enormous sports fandom. We think that changes faster than most people expect. Cricket cards are an obvious initial catalyst. IPL memorabilia is another. Recent regulatory changes around fantasy and real-money gaming are pushing consumer attention toward adjacent ways to engage with sports. The right India play is mobile-first, payments-native, and probably starts with cricket before broadening to Bollywood IP, regional language IP, and eventually global TCGs.

Across all of these regions, we think IP partnerships, trust, authentication, and payments are key bottlenecks to more commercial viability.

–

Zooming out, while there has been tremendous innovation in the last few years, we think the opportunity in collectibles is just beginning.

Collectibles have always had demand. They’ve always had emotional resonance, cultural relevance, and pockets of extreme value. What they haven’t had, until recently, is the infrastructure that allows markets to scale. Things like standardized grading, reliable price discovery, financing, and liquid marketplaces.

Sports and trading cards are simply the first place where all of those pieces have fallen into place. That same transition is starting to play out across watches, memorabilia, toys, and entirely new formats that didn’t exist five years ago. It’s happening across Asia-Pacific, across Latin America, and will also happen in markets that today feel underpenetrated.

We think massive businesses will emerge in collectibles around the “PSA for everything else”, digital packs / blind boxes for other categories, lending and financialization, and geographic expansion.

At Will Ventures, we’re excited about the next generation of innovation in the collectibles industry. If you’re building in this space, or thinking about it from a new angle, we’d love to hear from you.